Are you thinking of buying a home? You should know that the home buying process can be challenging, especially if this is your first time buying a home, so before buying your dream home you should first consider your budget, the neighborhood you will like to stay.

Home buying process is more than just visiting the homes. You also need to check your credit score and financing options, find the best deal and bargain, the realtor to work with, a home inspector to work with.

But wait a minute ask yourself the following questions, whether this is the right time for you to own your dream home

• How much house can I buy?

• Will I need to get a loan?

• Do I need a down payment?

• What desired neighborhood can I afford?

• Are home values in the neighborhood rising or falling?

In this post, we'll work you through all you need to know about the home buying process.

Knowing these steps will give you the confidence in buying your dream homes.

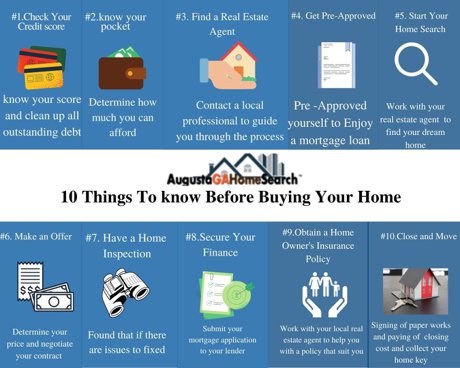

Here are the 10 things to know before buying your new home

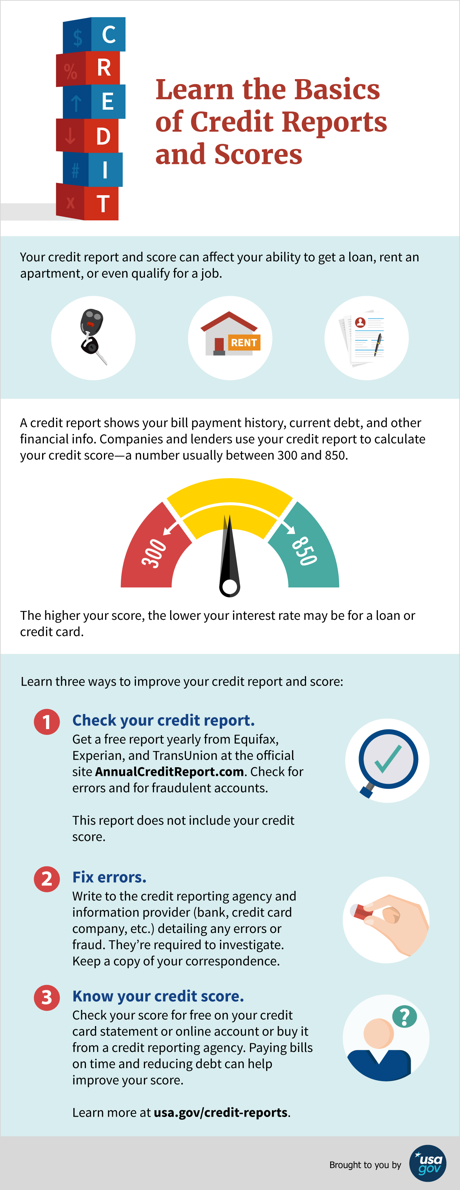

1. Check your credit score

Credit reports

Credit reports is a vital document that contains information about you, such information may include your workplace, current debt, crime history, bill payment history, loans and shown whether you have filed for bankruptcy

The credit report retrieve data from three main credit reporting agencies which are TransUnion, Equifax and Experian. Which is used to calculate your FICO score and your Vantage score.

The information in your credit report is used to calculate your credit score. It's based on the following factors:

· Payment history

· Outstanding balances

· Length of credit history

· Types of credit

Credit score: A number that ranges from 300-850.it shows information about your credit history. Your credit score number will help creditors to determine  whether to give you credit.

whether to give you credit.

Here are few benefits to having a good credit score of 700 above.

· Get Approval for Rental Houses and Apartments easily

· Allow you to Pay fewer Interest Rates on Loans

· Obtain Approved for Higher Limits

· Negotiating Power

· High Chance for Loan Approval

Considering getting a loan?

We have lenders for all types of loans FHA, VA, CONV, USDA, commercial and more

2. Determine how much house you can afford

Once you get pre-approved, your lender will tell you the maximum amount you’re able to borrow.

You have to take into consideration the following criteria such as your annual income, monthly debts and projected down payment amount

Know that your mortgage payment consists of four parts, known as, Principal, Interest, Taxes, and Insurance.

Principal and Interest

Principal and interest include your payments toward the loan balance and interest paid to your lender, this contains your basic mortgage payment

Taxes

As a property owner, you’re liable for paying annual property taxes to the local taxing authority. This Property taxes range from 1 to 2 per cent of your home’s value annually

Insurance

Before you can obtain a mortgage loan you need to insure your home. So no mortgage lenders will give you a loan without carrying insurance on your home.

Consider your budget to fit your taste

after you have come up with a rough budget of must-have home features. Your price point will likely dictate the size, location and amenities of your future home. Here are a few examples of wish list items to consider:

• Number of bedrooms and bathrooms

• Square footage

• Outdoor space

• Preferred location

• Type of home

• Layout, features and finishes

• School district

• Pet-friendliness

• Work commute

3. Find a real estate agent

A real estate agent is a professional who represents sellers or buyers of real estate or real property, An agent that is informed about the area you want to buy your home from will know the worth of the homes there, this will help you to avoid overpaying for a property.

Every neighborhood has its unique qualities that you want to be aware of before you buy.

Here are few things an agent can help you with.

Market insights

Helps to identify home value trends, new developments, buyer demand and the overall state of the market

Offer price

He finds out what a home is worth and recommends a competitive initial offer amount

Negotiating

Help to negotiate for a lower price and contingencies and repairs

Local familiarity

He has insider tips about the neighborhood and area schools

Professional recommendations

He provides referrals for a trusted lender, attorney, contractor or other vendors

Experience

He makes the process easy by handling hiccups, staying on top of due dates and overseeing paperwork

Choosing the right Realtor is a step to buying a home that should not be ignored.

Are you considering working with a professional realtor ?

Then Chris Samuel is the best choice for you.

Chris Samuel serve clients around the globe.

4. Get pre-approved

Before buying your home you need to get pre-approved, because this is very important in the home buying process, this means you should be able to get a loan if nothing changes about your credit score and financial situation.

You will need to get a pre-approval letter, this will help you compete with another buyer during the home buying process, a lot of sellers Make it compulsory that their buyers get pre-approved because this shows how qualified you are and give sellers confidence that you are not going to be turned down for a loan.

Lenders will verify your employment details, income levels and credit, for you to be pre-approved.

5. Start the home search

A lot of buyers including you starts their home buying process online with their first search. Start on Augustagahomesearch.com and search for homes in your target area, then filter by price and your must-haves. And also you can request an agent to send you listings.

6: Make an offer

At this stage, you have found your dream home, what next is for you to make an offer, the offer will be based on comparative market analysis and it is calculated based on the market value of comparable recent home sales in the same neighborhood. This will be done by your agent.

Your agent will help you to determine a fair price and advice you on possible terms for negotiation.

When making an offer is important to consider the following.

Contingencies

It is an agreement stating the conditions that need to be met before a sale can proceed, this agreement usually involves a seller and buyer ( you) or the lender and the buyer. When applying for mortgage loan your lender will demand appraisal contingency to ensure they’re not overpaying you.

Closing date:

Once you’ve decided to buy your home with a mortgage, the process will take 30-45 days after the contract is completed to close on the home, although you can request a later closing date that will suit your moving schedule when you submit an offer, keep in mind that the seller may reject your request.

Down payment

This is a sum of money you’re willing to put down when you make an offer, this will show that you are serious about buying the home.

7: Schedule the inspection

Home inspection is a process that uncovers issues with the home itself, it evaluates the home condition from the foundation to the roof, which is usually done by professionals. This will help you to make an informed decision about the home you’re considering buying.

This inspection is usually done within a week of the contract being signed, it is highly advisable for you to attend the inspection because this will reveal hidden information about the home.

8: Secure your financing

After you have been pre-approved, that is not the end you will have to submit your mortgage application to your lender and wait to receive ‘’ clear to close’’ this means your lender has officially approved your purchase.

9: obtain a homeowners insurance policy

If you’re a first time home buyer you will need the help of your lender to assist you to bring together a policy that can be paid through your escrow account monthly, because this policy will be needed to close on a home, you may ask your existing agent to help you get a policy that suits you if you’re not a first time home buyer.

10. Close and move

A day Before closing you will want to work around to see if the property looks the same as when you made your offer and also that the seller completed repairs if agreed on.

Once you are pleased with the property signing of paperwork and payments of the closing cost, which ranges from 3-5% of the sale price is expected to be pay by you. Once you pay both sellers and buyers have to sign and close the deal.

Finally, received your dream home key. You are now a legal owner of the house congratulation